Oilseed Rape market

Market Update for Rapeseed & Canola 24th of November 2025

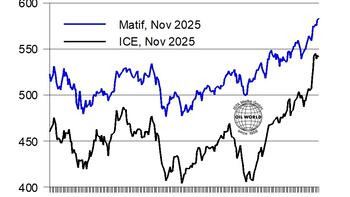

The price direction for the EU rapeseed market will be largely determined by the worldwide crush volumes, and thus primarily by the supply & demand fundamentals of the major vegetable oils on the world market. These are the latest trends outlined in the latest OIL WORLD monthly report:

Market Update for Rapeseed & Canola 20th of October 2025

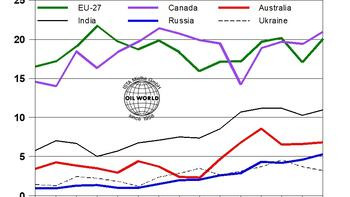

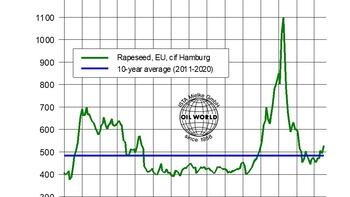

Record world production has exerted pressure on EU rapeseed prices in the first half of October. Larger than initially expected crops in Canada and Australia will more than offset the year-on-year setback in Ukraine, boosting world production of rapeseed & canola to a new high of 82.1 Mn T in 2025/26, up 6.5 Mn T from a year earlier. ...

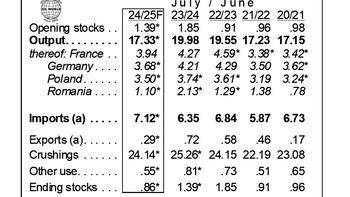

Market Update for Rapeseed & Canola 23th of July 2025

Update prepared by ISTA Mielke GmbH – Global Oil World analyses and forecasts for oilseeds, oils & fats and oilmeals in Hamburg, Germany. On www.oilworld.de more details are provided about the company profile and th...

Market Update for Rapeseed & Canola 30th of May 2025

The prospective recovery in world supplies of rapeseed & canola may turn out smaller than initially expected, pushing new-crop prices higher. This is primarily true in the three major exporting countries, viz. Canada, Australia and Ukraine, where smaller plantings and below-average yields (primarily Ukrai...

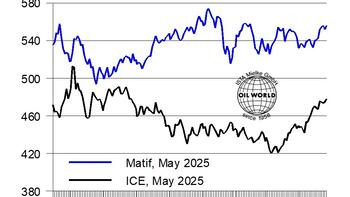

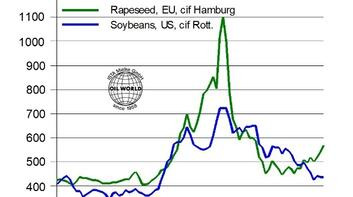

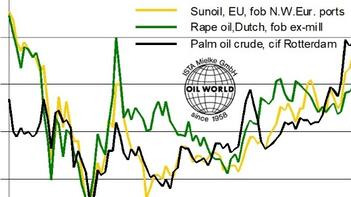

Market Update for Rapeseed & Canola 05th of May 2025

Seasonally declining supplies in the key producing countries as well as weather conditions and the pace of canola plantings in Canada and Australia for the 2025 crop, and geopolitical developments will be key price-determining factors in coming weeks, also affecting European rapeseed prices. The global rapese...

Market Update for Rapeseed & Canola 27th of March 2025

Diverging fundamentals in the two major markets, viz. the EU and Canada, have significantly widened the spread between genetically modified canola and non-GM rapeseed in March. Diminishing domestic supplies, primarily for crushers in Central Europe, pushed EU rapeseed prices higher so far this week. Nearby ra...

Market Update for Rapeseed & Canola 24th of February 2025

Diminishing supplies in the key producing countries as well as appreciating vegetable oil prices have pushed rapeseed & canola prices higher in the week to Feb 21, with Canadian canola prices on the ICE reaching a 7-month high of CAN-$ 680.10 in the May position on Feb 20. EU rapeseed prices followed the ...

Market Update for Rapeseed & Canola 20th of January 2025

Update prepared by ISTA Mielke GmbH – Global Oil World analyses and forecasts for oilseeds, oils & fats and oilmeals in Hamburg, Germany. On www.oilworld.de more details are provided about the company profile and th...

Market Update for Rapeseed & Canola 27th of Nov. 2024

Tightening supplies in Europe as well was rallying vegetable oil prices worldwide have pushed EU rapeseed prices higher in the cash and futures markets in November. Prices for nearby delivery in northern Germany reached US-$ 568 on average of Nov 1-21, up 13% since Aug 2024 and the highest monthly level since Feb 2023.

Market Update for Rapeseed & Canola 27th of May 2024

Bullish new-crop outlook is supporting rapeseed prices. The sizeable setback in EU rapeseed supplies as well as the prospective severe decline in Australian canola exports will force EU crushers to step up purchases of Canadian canola for delivery in 2024/25.

Market Update for Rapeseed & Canola 09th of April 2024

World market prices of rapeseed have recovered sizeably in March, supported by the rally in vegetable oil prices. Nearby prices in northern Europe reached $ 475 last month, up 5% from a month earlier but still trailing $ 519 in March 2023. Palm oil and soya oil were the price leaders upward in March with partly two-digit gains as a result...