Marekt Update for Rapeseed & Canola 5th of May 2026

Political uncertainty is likely to remain high in May, setting the stage for volatile commodity markets and complicating the transition from old- to new-crop supplies in the major oilseeds.

While by far the most concerning, the Iran war is not the only political factor that is affecting commodity markets at the moment. Announcements of further rising biofuel mandates in the US, Indonesia, Thailand and to a certain extent also in the EU have contributed to the strength in vegetable oil prices in April.

Market participants in the EU are now also closely monitoring weather developments in the key rapeseed producing regions. In its latest MARS report released on April 27, the EU Commission raised the forecast for average EU rapeseed yields, citing generally favorable crop conditions. However, dryness in parts of Germany, Poland, Hungary, the Czech Republic and the Baltics are reason for concern, potentially curbing yields below expectations.

EU Rapeseed vs. Canadian Canola in US-$/T

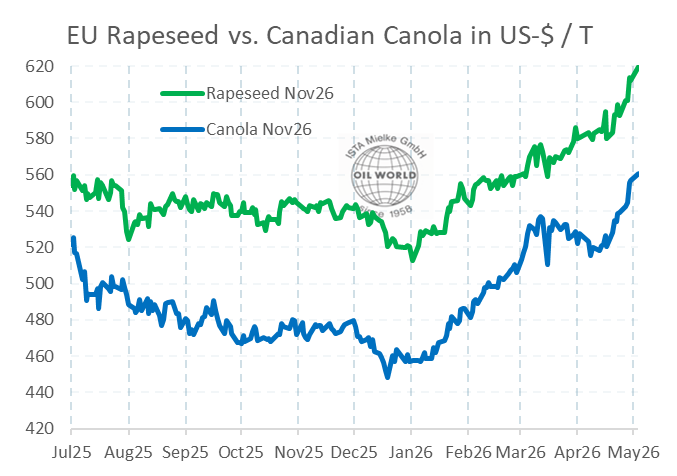

The other major price-determining factor for the rapeseed market is the prospective demand increase for rapeseed oil from EU biofuel producers. Following the escalation of the Iran war and the corresponding rally in energy prices, blending margins – at least on paper – already improved sizably in the past 6-8 weeks. New-crop rapeseed prices on the Matif (Nov position) reached a new contract high of EUR 529.50 at the close of May 4, up 3.5% on the week and 21% above Jan 2, 2026.

The German government has finally passed national law in line with the RED III regulation in April, ending double-counting for waste oils and raising the cap on cultivated biomass from the current 4.4% gradually to 5.8% by 2033. Similar to the situation in the US, biofuel producers stayed largely on the sidelines waiting for legislative certainty. Apart from the favorable policy changes in the EU and North America, the rapeseed market is currently benefiting from high prices of mineral oil and a comparatively high oil share, favoring processing margins of oilseeds with a high oil content.

With the current season nearing completion in most of the key countries (except for Australia), production prospects for 2026/27 have become a major price-making factor. Considering the fact that imports usually satisfy 25-30% of the requirements of EU rapeseed crushers, developments in the key exporting countries are a crucial component for the supply and price outlook for 2026/27. It is still highly uncertain how much acreage farmers in Canada and Australia will switch from grains – which require considerably more fertilizer – to canola but the shift could be substantial. The likelihood of El Niño developing in coming months may jeopardize Australian canola production in 2026/27. It is still early in the season but we consider it likely that lower average yields will more than offset the prospective increase in canola plantings. OIL WORLD forecasts the global area of rapeseed & canola to increase by 1.7 Mn ha in 2026/27, of which +0.5 Mn ha in Canada, +0.3-0.4 Mn ha in Australia and +0.25 Mn ha in the EU-27.

Update prepared by ISTA Mielke GmbH – Global Oil World analyses and forecasts for oilseeds, oils & fats and oilmeals in Hamburg, Germany. On www.oilworld.de more details are provided about the company profile and the individual services.

Quelle: ISTA Mielke GmbH