Market Update for Rapeseed & Canola 07th of July 2024

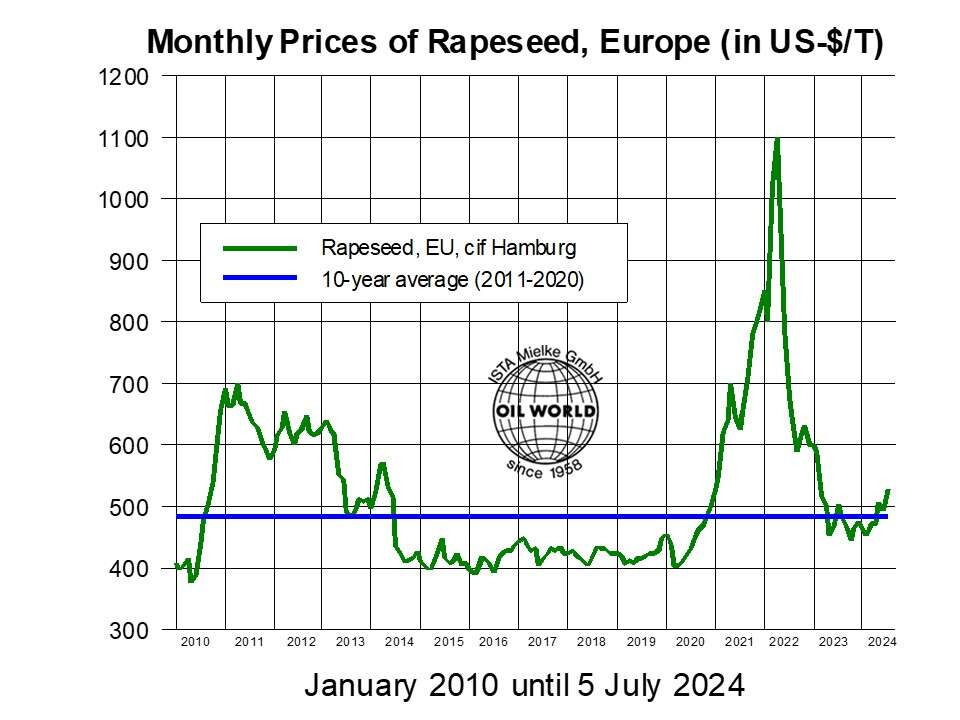

EU rapeseed prices recovered sharply in the week to July 5, supported by the bullish supply outlook for 2024/25 as well as soaring vegetable oil prices.

Reports about excessive rainfall in parts of Europe ahead of harvest operations contributed to the price strength. Nearby quotations in Germany exceeded 490 EUR or US-$ 530 last week, up 7% in two weeks and the highest level since May 2024. Thus, this year’s new-crop price pressure, with harvesting now gaining momentum across the key growing regions, appears to be short-lived.

Rapseed prices since 2010

Independent price strength in the EU is inevitable to attract sufficient volumes of rapeseed & canola on the world market to offset the sizeable decline in domestic supplies in July/June 2024/25. This is now being reflected in the deferred positions on the futures markets, with the premium of EU rapeseed vis-a-vis Canadian canola (both Nov position) exceeding US-$ 70 in the week to July 5 compared to only $ 45 a month ago and the discount of $ 78 on July 6, 2023 (in the respective Nov 2023 contracts).

World exports rapeseed & canola have exceeded the year-ago level by more than 40% in Apr/June 2024, with by far biggest increases in Canada and Australia. Combined shipments from Ukraine, Canada, Uruguay and Australia increased by 0.8 Mn T or 37% in Apr/May, followed by ongoing large exports according to preliminary trade information. The EU was the by far largest destination at 0.9 Mn T (vs. 0.2 Mn T in Apr/May 2023), accounting for 30% of the total.

Large disposals indicate that this season’s Australian canola production and probably also the 2022 crop turned out larger than initially expected. Latest official trade data show canola exports of 0.68 Mn T in May (vs. 0.5 Mn T a year earlier). Another 0.4-0.5 Mn T have reportedly been shipped in June (vs. 0.32 Mn T a year earlier). OIL WORLD now estimates the 2023 canola crop at 5.75 Mn T compared to the latest ABARES number of 5.52 Mn T and their revised estimate of 8.4 Mn T for 2022 (vs. 8.27 Mn T ABARES).

Rapeseed prices are also supported by the prospective production deficit in vegetable oils in 2024/25. In the ANNUAL 2024, OIL WORLD forecasts ample supplies of soybeans while supplies of high oil-yielding oilseeds will likely be insufficient. A relatively small growth in world palm oil production is further raising the dependence on soya oil next season. Global supplies of sunflowerseed and rapeseed are currently forecast to decline by a combined 4 Mn T in 2024/25, following the year-on-year increases in crushings of the two soft seeds by a staggering 18 Mn T in the past two season combined.

Update prepared by ISTA Mielke GmbH – Global Oil World analyses and forecasts for oilseeds, oils & fats and oilmeals in Hamburg, Germany. On www.oilworld.de more details are provided about the company profile and the individual services.