Market Update for Rapeseed & Canola 08th of September 2025

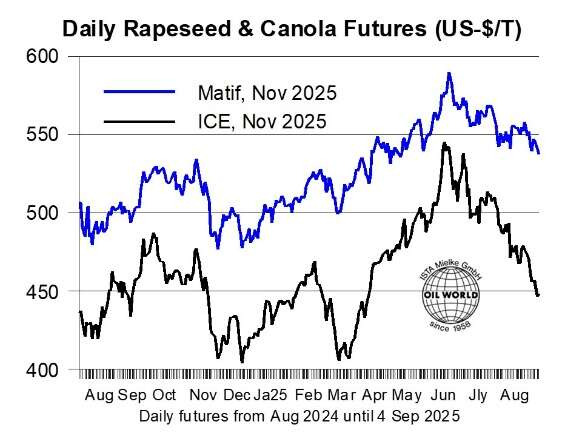

Canola futures prices in Canada declined by more than 8% in four weeks to Sept 4, reducing the premium over soybeans and widening the discount versus European rapeseed.

Harvesting has only started in Canada but there is growing confidence that this year's crop will exceed initial expectations. This comes on top of recovering production in the EU and another large crop shaping up in Australia.

Daily Rapeseed & Canola Futures (US-$/T)

This year’s Canadian and Australian canola crops were off to a bad start with partly severe dryness during planting and early crop development in the key growing regions. However, widespread rainfall was registered in recent weeks, replenishing soil moisture supplies and improving yield prospects in both countries. World production is now estimated at 80.2 Mn T in 2025/26, up 2.2 Mn T from our previous estimate and sharply above 75.4 Mn T achieved last season. However, stocks at the start of the season were an estimated 4.1 Mn T lower, limiting the year-on-year increase in world supplies of rapeseed & canola to 0.7-0.8 Mn T.

Larger than expected global supplies of rapeseed & canola coincide with China's de facto import ban on rapeseed and products from Canada. The recent price erosion severely hurts Canadian farmers, prompting the Canadian government to announce support measures. In contrast, processors in Canada are benefiting from low canola prices. Recovering US demand for canola oil is putting them in a position to sell canola meal aggressively in Europe, the US and elsewhere, offsetting the loss of the Chinese market at least partly. The Canadian canola market is thus looking for ways to cope with the ongoing trade conflicts via price concessions, similar to the US soybean market.

Volatility is likely to persist – or may even intensify – in the rapeseed complex during the 2025/26 season. There are currently strong indications that political interventions will continue to hamper the market’s primary function of aligning world supply and demand fundamentals via price changes. Price developments on the world market will significantly influence prices paid to the rapeseed farmer in the EU.

Unresolved and partly intensifying trade conflicts are expected to have severe repercussions on global trade flows this season. This is primarily true for China, for which OIL WORLD expect imports of rapeseed & canola to plummet by more than 40% in July/June 2025/26, assuming that at least part of the prospective severe decline in imports of Canadian canola (following the implementation of a 76% import duty this month) will be replaced by Australia. The latest decision of the Chinese government to block also Canadian canola comes on top of the 100% import duties on Canadian canola oil and meal, which is seen keeping Canadian canola crushings below potential in 2025/26.

Political intervention may also change trade flows between the EU and Ukraine this season. A 10% export tax on both rapeseed and soybeans came in force on Sept 4 but the actual effect on export volumes will probably be limited as “agricultural producers” are excluded, which creates a loophole for agroholdings. In contrast, farmers and multinational companies are reportedly subject to the duty, complicating marketing of this year’s Ukrainian rapeseed crop (a large part of which still unsold).