Market Update for Rapeseed & Canola 18th of December 2025

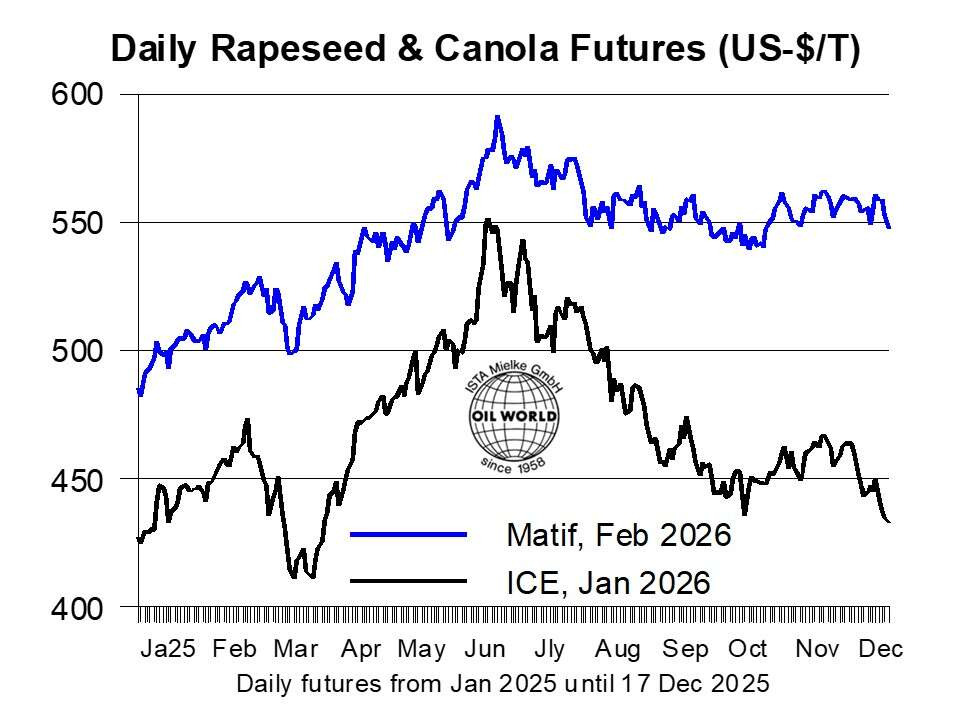

Weakness in vegetable oil prices as well as disposal problems in Canada and the corresponding setback in canola prices have pressured European rapeseed prices in the first 2 weeks of December.

The bearish sentiment on the world market is thus offsetting the bullish impact of the German Government’s decision to end double counting for certain biodiesel feedstocks in 2026. However, the prospective increase in rapeseed oil usage as well as the slowing down of the growth in world vegetable oil production is seen supporting EU rapeseed prices in coming months.

Futures Matif Winnipeg

Exceptional high yields have been confirmed in Canada and Australia, boosting combined canola production in the two major exporting countries by 3.1 Mn T or 12% from a year earlier in 2025/26. OIL WORLD raised its Canadian production estimates to 21.8 Mn T (vs. 19.4 Mn T in 2024) and 7.4 Mn T in Australia (vs. 6.7). Upward revisions also became necessary in India and Russia, bringing world production of rapeseed & canola to a new high of 84.9 Mn T in 2025/26, up 8.7 Mn T from a year earlier. However, world exports of rapeseed are estimated to have plummeted by 3.4 Mn T in July/Nov 2025, illustrating the severe impact of political interference on trade flows, which has made an already complex market even more difficult for farmers to navigate.

This is primarily true for Canadian canola producers who are currently struggling to find a home for this year’s record crop. Virtually no sales to China so far this season following the implementation of prohibitively high import duties reduced Canadian canola exports by about 1.6 Mn T or more than 40% in the first four months of the Aug/July 2025/26 marketing year. Ukrainian farmers are faced with export restrictions, implemented to support the domestic crush industry. However, this measure also forced farmers to sell their rapeseed on the domestic market at prices below those offered by European crushers. Ukrainian rapeseed exports declined by more than 50% to a multi-year low of 1.22 Mn T in July/Nov 2025, of which 95% earmarked for the EU-27.

German rapeseed oil usage is expected to rise in 2026, following the decision of the German government to end double counting for advanced biofuel feedstock, viz. used/waste oils, as part of the national biofuel guidelines under the RED III directive of the European Commission.

The main goal of the 118-page document is to raise the share of “Renewable Fuels of Non-Biological Origin” (RFNBO) in the total energy mix to reach the greenhouse gas emission savings in 2040 set by RED III. However, the relevance of these fuels is still limited, raising demand for rapeseed oil and other conventional feedstock for biodiesel in the near to medium term. Stricter rules concerning the sustainability certification of feedstock are likely to also raise the share of rapeseed oil in biodiesel. This follows large imports of UCO, which according to market participants were partly fraudulent, in recent years. German rapeseed oil usage reached an estimated 3.2 Mn T in Oct/Sept 2024/25, accounting for roughly 30% of the EU total.

Following the setback of 0.3 Mn T in Oct/Sept 2024/25, European rapeseed oil usage is seen rebounding this season. The extent of the recovery is likely to be determined by the relative price development of rapeseed oil vis-a-vis other vegetable oils in coming months.

Quelle: ISTA Mielke GmbH