Market Update for Rapeseed & Canola 20th of January 2025

Update prepared by ISTA Mielke GmbH – Global Oil World analyses and forecasts for oilseeds, oils & fats and oilmeals in Hamburg, Germany. On www.oilworld.de more details are provided about the company profile and the individual services.

The price changes of the last few months are partly foreshadowing developments shaping up in the further course of this season. Despite the current drought in parts of South America, the global supply of soybeans will be more than sufficient to meet demand this season. This will continue to put pressure on soybean meal as well as soybean prices.

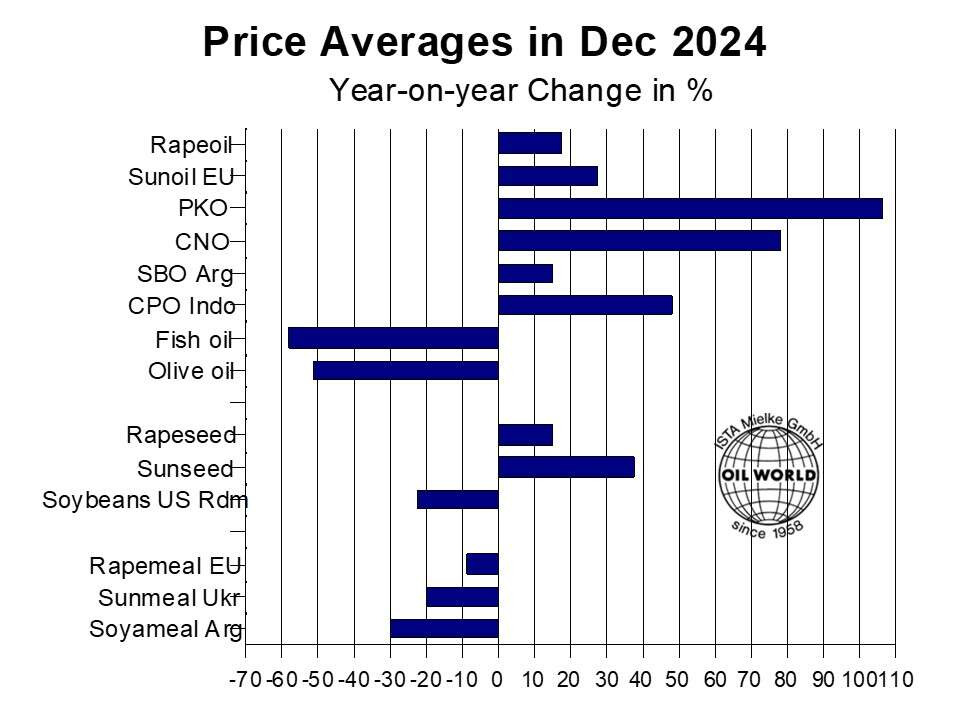

In contrast to soybeans, the prices of rapeseed and even more so of sunseed have risen significantly in 2024 as a result of massive declines in world production. Rapeseed meal and sunflower meal therefore followed the downward trend in soybean meal prices only at a distance.

Price averages in Dec 2024

EU rapeseed crushers will increasingly rely on large imports of Canadian and Australian rapeseed in Jan/June 2025 to make up for insufficient domestic supply. The significant shortage of supply in the EU should support the rapeseed price in the EU in the remaining months of the season.

2025/26: European rapeseed production in 2025 is likely to recover sizeably from 2024, but stay below potential, following lower than initially expected winter rapeseed plantings in key producing countries. This is primarily true for Germany and France were rapeseed plantings at best stagnated at a combined 2.4 Mn ha last autumn while preliminary data indicate a further reduction of more than 10% in Denmark.

The 7-8% decline in average EU rapeseed yields in 2024, rising costs and subdued rapeseed prices of EUR 450-470 in Northwest Europe shortly before plantings apparently prompted farmers to switch to other crops. Partly detrimental weather conditions additionally hampered plantings.

In contrast, Eastern European farmers stepped up plantings, with the area in Romania seen increasing by roughly 30% to an estimated 600 Thd ha. Sizeable year-on-year increases from last year’s reduced levels are also expected for Bulgaria, Estonia, Latvia, Hungary and Croatia, bringing the total European rapeseed area to an estimated 5.95 Mn ha, up 0.31 Mn ha or 6% on the year but still 5% below 2023.

Following two consecutive declines in average EU yields, we expect rapeseed production per hectare to recover to 3.2 T/ha in 2025, up from 3.0 T/ha in 2024 but still below 3.34 T/ha in 2022. This estimate is based on about normal weather conditions in the remaining six months of the growing season.

OIL WORLD tentatively forecasts EU-27 rapeseed production to recover to 19.1 Mn T in 2025, up 2.2 Mn T from a year earlier but still trailing the crops of 20.2 Mn T and 19.6 Mn T in the preceding two seasons. However, sharply lower stocks as of end-June 2025 are likely to keep EU rapeseed supplies relatively tight and import demand elevated in July/June 2025/26.