Market Update for Rapeseed & Canola 20th of October 2025

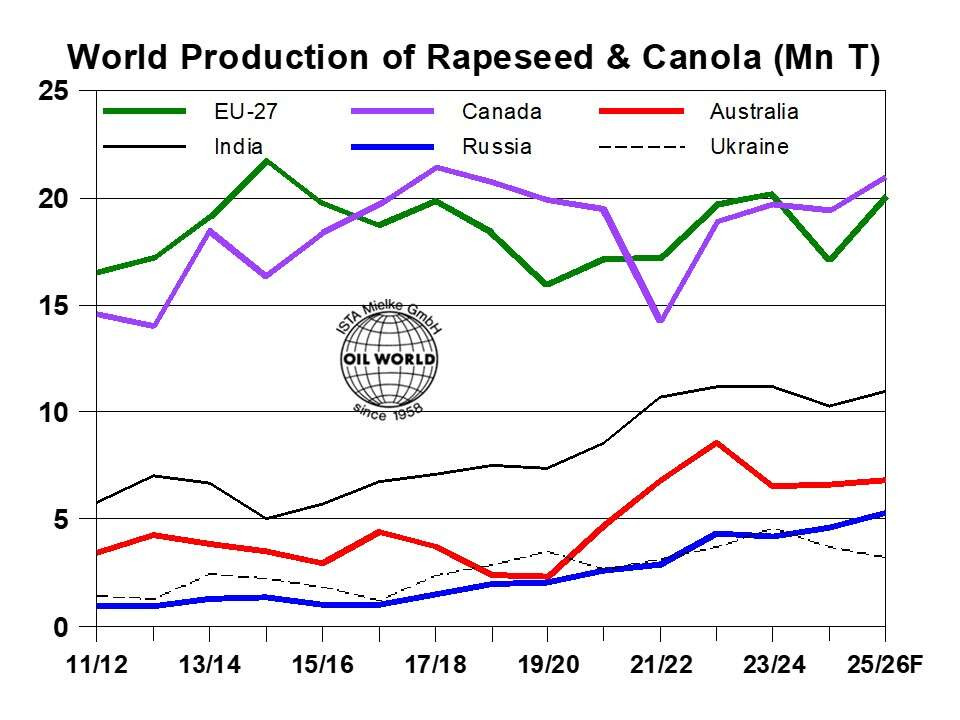

Record world production has exerted pressure on EU rapeseed prices in the first half of October. Larger than initially expected crops in Canada and Australia will more than offset the year-on-year setback in Ukraine, boosting world production of rapeseed & canola to a new high of 82.1 Mn T in 2025/26, up 6.5 Mn T from a year earlier.

OIL WORLD expects a Canadian crop of at least 21.0 Mn T this year, implying a year-on-year increase of 1.6 Mn T. In contrast, Canadian canola disposals plummeted on the year in the first two months of the 2025/26 season owing to the still unresolved trade conflict with China and insufficient purchases from other countries. Canola production is seen exceeding demand this season, keeping Canadian canola prices on the defensive, with veg. oil demand developments in the US – in particular the final biofuel legislation for 2026 – a key price-determining factor to watch.

World Production of Rapeseed & Canola (Mn T)

Sharply reduced stocks carried into the season will limit the recovery in world supplies to 2.7 Mn T in 2025/26. But it remains to be seen whether these large world supplies will raise rapeseed & canola crushings accordingly in the 2025/26 season. Escalating trade conflicts (primarily China/Canada) and other forms of government interventions, viz. Ukrainian export duties, have severely impacted global trade flows in recent months, keeping imports and processing in the key countries (primarily China) below potential.

Combined rapeseed & canola exports from Ukraine, Canada and Australia (accounting for 85% of the total in Jan/Dec 2024) plummeted to only an estimated 2.5 Mn T in July/Sept 2025, down more than 50% from a year earlier. While heavily frontloaded disposals in Oct/June 2025/26 and the corresponding reduction of domestic canola stocks reduced exports from Australia by roughly 0.7 Mn T from a year earlier last quarter, the reasons for the severe declines in Canada and Ukraine were mainly political. Escalating trade tensions with China slashed Canadian canola exports by an estimated 1.1 Mn T in July/Sept, while the implementation of a 10% export tax curbed shipments from Ukraine to 0.86 Mn T (vs. 1.83 Mn T in July/Sept 2024).

Abundant Canadian export supplies are seen reviving purchases from EU crushers this season, potentially taking market share from EU farmers. However, rapeseed prices are likely to be supported by lower than initially expected sunflowerseed production, primarily in the Black Sea region. In addition, vegetable oil import requirements are expected to increase in the season 2025/26 in some key countries. Reduced sunflower oil supplies come on top of the prospective decline of soya oil exports, raising demand for rapeseed oil.

Quelle: ISTA Mielke GmbH