Market Update for Rapeseed & Canola 27th of March 2025

Diverging fundamentals in the two major markets, viz. the EU and Canada, have significantly widened the spread between genetically modified canola and non-GM rapeseed in March. Diminishing domestic supplies, primarily for crushers in Central Europe, pushed EU rapeseed prices higher so far this week. Nearby rapeseed futures on the Matif (May position) closed at EUR 506 on March 25, up 9% from the recent low of EUR 466 on March 17 but still 5% down from a month ago.

Last year’s reduced EU rapeseed crop (down 3.3 Mn T), smaller old-crop stocks carried into the 2024/25 season (down 0.4 Mn T) as well as relatively high crushings in July/Dec 2024 will make demand-rationing inevitable in the remainder of the season. We currently estimate EU rapeseed crushings to decline by 1.4 Mn T in July/June 2024/25, with virtually all of the setback expected to occur in Jan/June 2025.

In contrast, Canadian canola supplies may turn out more ample than initially expected, in view of the currently escalating trade disputes with Canada’s two largest trading partners, viz. China and the US. There are still a lot of uncertainties regarding the timing and magnitude of the announced or threatened trade restrictions. Will US President Trump again postpone the implementation of the announced 25% import duty on Canadian goods after the current 30-day extension of the deadline? Will China also implement import duties on Canadian canola in line with the 100% duty on canola oil and meal or will they take advantage of the current relatively low canola prices and expand domestic crushings? The answers to these questions will also have a massive impact on rapeseed prices in the EU in coming weeks.

While relatively tight world export supplies of vegetable oils should make it rather easy to revive import demand for Canadian canola oil in countries other than China and the US in coming months, the situation in meal is more complex. China and the US are the key outlets for Canadian canola meal, together receiving virtually all of the record 5.8 Mn T exported in Jan/Dec 2024. The uncertain prospects for exports to both countries and the limited demand potential in the rest of the world are seen keeping Canadian canola crushings below potential in Apr/July 2025.

Limited export supplies of rapeseed & canola in the rest of the world are likely to shift at least part of the EU import requirements to Canada in Apr/June. The widening of the price premium of EU rapeseed vis-a-vis Canadian canola, in the nearby position increasing to US-$ 143 at the close of March 25 (vs. $ 113 a week earlier and only $ 65 on Feb 10), will also promote additionally sales.

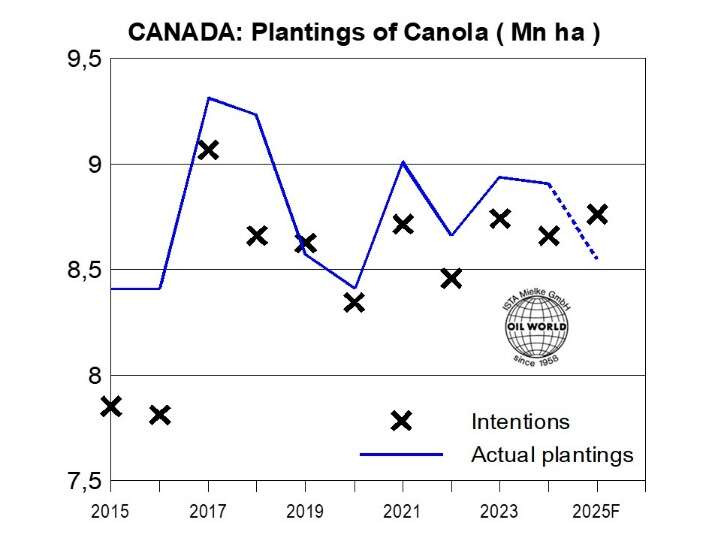

Planting area of Rapseed in Canada

Outlook 2025/26: Uncertain demand prospects and deteriorating profit margins are likely to keep Canadian canola sowings below potential in 2025. OIL WORLD currently forecasts Canadian canola sowings to decline to a 5-year low of only 8.55 Mn ha this year (vs. 8.91 Mn ha in 2024), falling below Statistics Canada’s planting intentions for the first time since 2019.

Update prepared by ISTA Mielke GmbH – Global Oil World analyses and forecasts for oilseeds, oils & fats and oilmeals in Hamburg, Germany. On www.oilworld.de more details are provided about the company profile and the individual services.