Market Update for Rapeseed & Canola 29th of June 2026

The stage is set for a bullish price outlook for vegetable oils in the next 12 months. OIL WORLD’s first forecast for the 2026/27 season points to a global production deficit of 17 oils & fats as well as to inevitable demand rationing and higher prices. The global vegetable oil market will be torn between booming demand from the biofuel sector and supply woes.

Palm oil is likely to be the price leader upward in July/June 2026/27 due to 1) a prospective decline in production, 2) rising domestic palm oil consumption in the producing countries (biodiesel) and 3) an even sharper reduction of palm oil exports. This is seen rising dependence on seed oils and a resulting further sizable increase in oilseed crushings as well as ample supplies of oilmeals, resulting in deviating price trends. Rapeseed prices are set to benefit from the looming shortage of vegetable oil, with average prices in northern Germany in July/June 2026/27 forecast to increase by 5-10% from US-$ 570 registered in 2025/26.

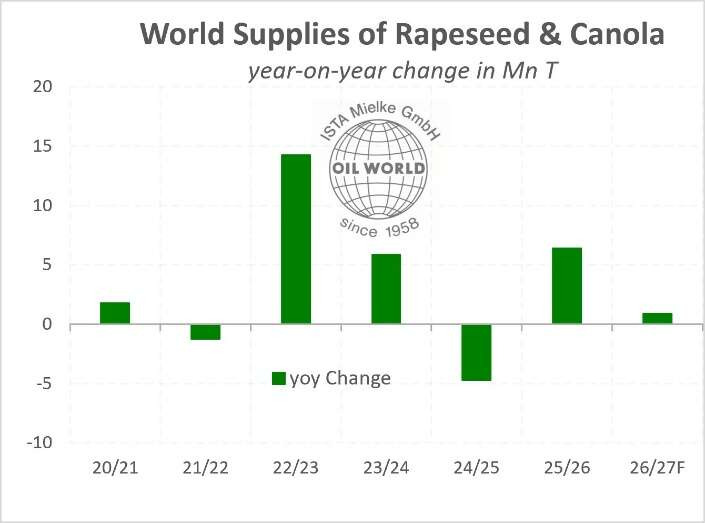

World Supplies of Rapeseed & Canola

Relatively high returns per hectare have prompted farmers worldwide to step up rapeseed plantings for the 2026/27 crop, primarily at the expense of grains. OIL WORLD forecasts the global harvested area of rapeseed & canola at a new high of 42.3 Mn ha next season, up 1.6-1.7 Mn ha from a year earlier and 10 Mn ha or 32% above 2019/20. The by far biggest increase is shaping up in Canada (up 0.5 Mn ha), followed by the EU-27 (+0.3 Mn ha), Australia and the US (each +0.2 Mn ha).

World production of rapeseed & canola is forecast to reach a new high of 86.1 Mn T in 2026/27, implying a slowdown of the year-on-year growth to 0.3 Mn T compared to an increase of 9.3 Mn T a year earlier. However, larger stocks at the beginning of the season will raise world supplies by 0.9 Mn T on the year.

EU rapeseed production is estimated to increase by 0.3-0.4 Mn T to a new high of 20.9 Mn T in 2026. However, competition for the reduced world export supplies is seen increasing in July/June 2026/27, potentially reducing EU imports of rapeseed & canola to 6.5-6.6 Mn T, down sharply from 7.0 Mn T and 8.2 Mn T in the preceding two seasons. EU imports from Ukraine are likely to stagnate or at best marginally increase to 1.8 Mn T in July/June 2026/27. Soaring domestic requirements and a resumption of Chinese purchases of Canadian canola will reduce EU imports from Canada. This will require EU imports of at least 3.3-3.4 Mn T from Australia in 2026/27 (up 0.5 Mn T from a year earlier), making Australian weather conditions in coming months a key factor to watch.