Market Update for Rapeseed & Canola 30th of March 2026

Rising energy prices are pushing vegetable oil markets to multi-year highs – with direct implications for rapeseed. While biodiesel and HVO are gaining significant competitiveness, it remains uncertain how strongly demand for vegetable oils in the energy sector will increase. At the same time, this bullish demand outlook is meeting record global rapeseed supplies. Between the energy market rally, geopolitical uncertainties, and shifting planting decisions, the market is heading into a highly dynamic season – with sunflower potentially emerging as a key winner.

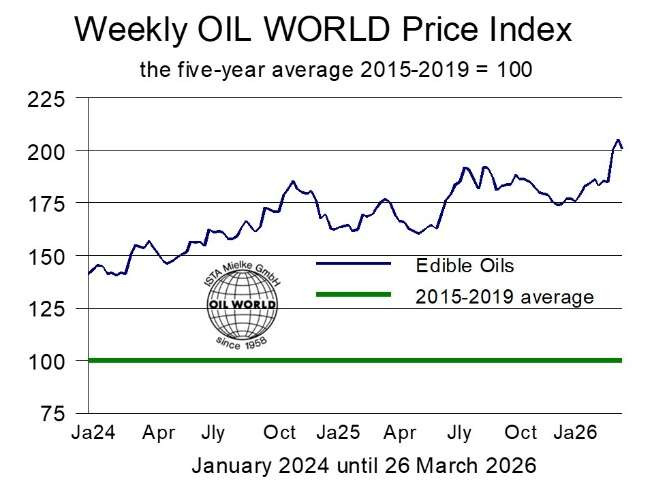

Soaring energy prices have pushed vegetable oil prices to the highest level in more than 3 years in March. The OIL WORLD price index of edible oils reached 205 points in the third week of March and eased slightly to 201 points in the week to March 26 compared with 177 points at the end of March 2025. It is the highest level since June 2022 (224 points shortly after the Russian invasion in Ukraine).

Weekly Oild World Price Index

However, vegetable oil prices have followed the price appreciation in the energy market only hesitatingly. As a result, biodiesel and HVO have significantly improved their competitiveness relative to mineral diesel, but it is unclear how quick and to what extent this will lead to increased consumption of vegetable oils for energy in the individual countries. Most of the focus is now being placed on Indonesia, Brazil, the European Union and the USA.

Rapeseed prices are currently torn between the bullish demand outlook for rapeseed oil as a feedstock for biofuel, following the rally in global energy prices so far this month, and record world supplies this season. OIL WORLD estimates world production of rapeseed & canola to reach 85.6 Mn T in 2025/26, a new high and 9.4 Mn T above the reduced year-ago level. Most of the increase was registered in the EU-27 and Canada, with the latter driven by exceptionally high yields of 2.5 T/ha compared to 2.2 T/ha achieved in 2024. However, further increases also occurred in South America, where farmers are taking advantage of comparatively high prices of high oil-yielding oilseeds.

Reduced old-crop stocks carried into the 2025/26 season (primarily in Canada) somewhat offset the sizeable increase in production, but world supplies of rapeseed & canola still reached a new high of an estimated 97.9 Mn T, up 6.2 Mn T from a year earlier and sharply above 76.6 Mn T in 2021/22.

Market participants are assessing the potential repercussions on the Iran war on energy, transportation and production costs. Higher fuel and fertilizer prices will influence the planting decisions of farmers in coming months. The acreage devoted to soybeans and sunflowerseed is likely to be increased at the expense of other crops (primarily corn) which require considerably more fertilizer inputs.

When it comes to plantings in the northern hemisphere this spring, sunflowers will be a preferred crop for many farmers. OIL WORLD forecasts the global area under sunflowerseed to be increased further to a new high of 34.1 Mn ha in 2026/27 on top of last year’s unusually high 32.8 Mn ha. Production prospects are highly dependent on weather conditions. If we assume about normal weather, sunflowerseed production could reach 62-63 Mn T in 2026/27, a record high and substantially above the 56.9 Mn T in 2025/26 and the previous high of 59.4 Mn T in 2023/24.

Quelle: ISTA Mielke GmbH