Market Update for Rapeseed & Canola 30th of May 2025

The prospective recovery in world supplies of rapeseed & canola may turn out smaller than initially expected, pushing new-crop prices higher. This is primarily true in the three major exporting countries, viz. Canada, Australia and Ukraine, where smaller plantings and below-average yields (primarily Ukraine) may reduce combined output by 0.8-0.9 Mn T this year.

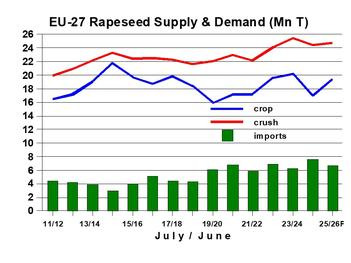

In contrast, OIL WORLD forecasts the EU rapeseed crop to recover by 2.5 Mn T this year (vs. the setback of 3.2 Mn T in 2024), following larger than initially expected plantings and assuming a recovery in average yields from last year’s unusually low levels in most production regions. However, the extent of the recovery in average yields still hinges on weather developments in the next 4-6 weeks. But even a crop of 19.4 Mn T will be insufficient to satisfy the requirements of EU crushers, keeping EU import demand elevated in July/June 2025/26.

We forecast EU imports of rapeseed & canola to reach 6.6 Mn T in July/June 2025/26, of which 2.5-2.6 Mn T from Ukraine, 2.5 Mn T from Australia and 1.1 Mn T from Canada. This estimate is based on the assumption that EU prices strengthen relatively to Canadian canola in the course of the 2025/26 season.

World rapeseed crushings have exceeded expectations in recent months. We have raised our estimate for July/June 2024/25 to 77.2 Mn T, up 0.8 Mn T from our estimate a month ago but still 0.6 Mn T below the year-ago level. But at 77.2 Mn T OIL WORLD forecasts processing to exceed world production of rapeseed by 1.7 Mn T this season, reducing the stocks to a three-year low. Lower stocks carried into the 2025/26 season will make the rapeseed market vulnerable to a price rally if any weather-related production concern in one of the key growing regions emerge in coming weeks.

The OIL WORLD price index of eight edible oils peaked this season already in November and has again been on a downtrend since early April. The bullishness initially emanating from declining production of sunflower oil, rapeseed oil and palm oil has been eased of late by declining biodiesel/HVO production, primarily in the USA, the EU-27, Argentina and China, which lowered feedstock requirements. Low mineral oil prices have hurt the competitiveness of vegetable oil-based biofuel in recent months.

These developments are seen curbing the growth of total world consumption of eight major vegetable oils to only 0.6 Mn T in Oct/Sept 2024/25, compared to 8.7 Mn T last season. A decline of consumption by 1.5 million to 24.5 Mn T is currently considered likely in the EU-27, limiting the rally in rapeseed oil prices despite relatively tight EU supplies.

Update prepared by ISTA Mielke GmbH – Global Oil World analyses and forecasts for oilseeds, oils & fats and oilmeals in Hamburg, Germany. On www.oilworld.de more details are provided about the company profile and the individual services.